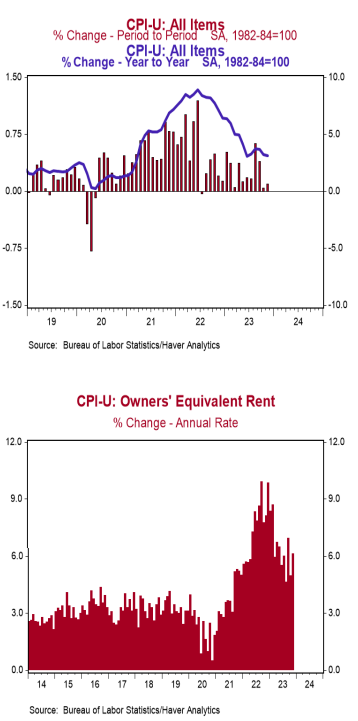

- The Consumer Price Index (CPI) rose 0.1% in November, above the consensus expectation of no change. The CPI is up 3.1% from a year ago.

- Energy prices declined 2.3% in November, while food prices rose 0.2%. The “core” CPI, which excludes food and energy, rose 0.3% in November, matching consensus expectations. Core prices are up 4.0% versus a year ago.

- Real average hourly earnings – the cash earnings of all workers, adjusted for inflation – rose 0.2% in November and are up 0.8% in the past year. Real average weekly earnings are up 0.5% in the past year.

Implications: There seems to be a widespread belief that inflation is in the rearview mirror, but today’s consumer price index suggests that, at this point, this is wishful thinking. Consumer prices rose 0.1% in November while the twelve-month comparison ticked down to 3.1%. That is leaps and bounds better than the 7.1% reading in the year ending November 2022, but still not close to the Fed’s 2.0% long-term target. Overall prices were once again held down by volatile energy prices, which fell 2.3% in November due to lower prices for gasoline (-6.0%). Stripping out energy and its often-volatile counterpart – food prices (+0.2% in November) – “core” prices rose 0.3% while the twelve-month comparison remained a worrisome 4.0%. That is not a huge improvement versus the 6.0% reading in November 2022. Taking a deeper look under the inflation hood reveals more concern. Rental inflation – both for actual tenants and the imputed rental value of owner-occupied homes – continues to run hot, up 0.5% for the month and running close to or above a 6% annualized rate over three-, six-, and twelve-month timeframes. Meanwhile, a subset category of prices that the Fed is watching closely – known as the “Super Core” – which excludes food, energy, other goods, and housing rents, jumped 0.4% in November. This measure is up 3.9% in the last twelve months but has been accelerating of late; up at a 5.2% annualized rate in the last three months. Although inflation is generally trending lower it is still not where the Fed wants it to be. With interest rates now above inflation across the yield curve and the M2 measure of the money supply down 4.5% from the peak in July 2022, money is tight enough to bring inflation down. More important, we continue to believe that a monetary policy tight enough to bring inflation down is also tight enough to induce an eventual recession. How the Federal Reserve responds to that economic weakness could determine whether we repeat the inflationary 1970s.