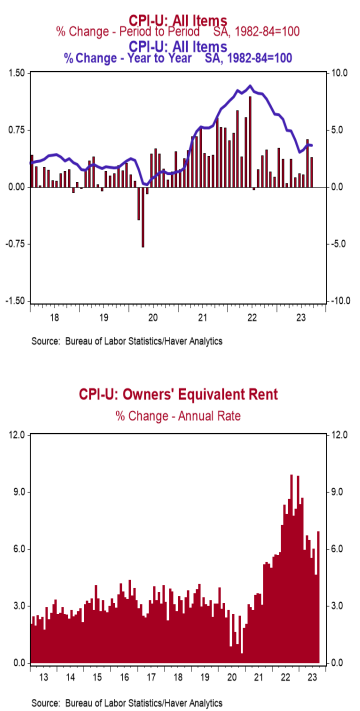

- The Consumer Price Index (CPI) rose 0.4% in September, above the consensus expected +0.3%. The CPI is up 3.7% from a year ago.

- Energy prices rose 1.5% in September, while food prices increased 0.2%. The “core” CPI, which excludes food and energy, rose 0.3% in September, matching consensus expectations. Core prices are up 4.1% versus a year ago.

- Real average hourly earnings – the cash earnings of all workers, adjusted for inflation – declined 0.2% in September, but are up 0.5% in the past year. Real average weekly earnings are down 0.1% in the past year.

Implications:

The Federal Reserve’s fight against inflation is not over. Consumer prices rose 0.4% in September, coming in above the consensus expectation, while the twelve-month comparison held steady at 3.7%. Inflation has re-accelerated of late, with consumer prices up 4.9% at an annualized rate in the last three months. Part of the recent run-up in prices is due to the volatile energy sector, which rose 1.5% in September after increasing 5.6% the month prior. But with a depleted Strategic Petroleum Reserve and escalating geo-political tensions in Ukraine – and now Israel – energy prices may remain a tailwind for inflation as we close out 2023. A deeper dive under the inflation hood confirms the Fed’s battle is not over. “Core” prices – which exclude the effects of the typically volatile food and energy sectors – rose 0.3% for the month and are up 4.1% in the last twelve-months. Rental inflation – both for actual tenants and the imputed rental value of owner-occupied homes – continues to run hot, up 0.5% for the month and running close to or above a 6% annualized rate over three-, six-, and twelve-month timeframes. Meanwhile, a subset category of inflation that the Fed is watching closely – known as the “Super Core” – which excludes food, energy, other goods, and housing rents, jumped 0.6% in September. This measure is up 3.8% in last twelve months but has been accelerating of late; up at a 4.8% annualized rate in the last three months. No matter which way you cut it, inflation remains nowhere close to where the Fed wants it to be. Couple that with a resilient US labor market, Powell and Co. still have plenty of reason to keep monetary policy tight in the months to come. The worst part of today’s report was that real average hourly earnings declined 0.2% in September, taking a bite out of consumer spending power. As for the economy, we continue to believe a recession is on the way. Equity investors should remain vigilant as we navigate these unprecedented times. In employment news this morning, initial claims for jobless benefits were unchanged last week at 209,000. Continuing claims rose 30,000 to 1.702 million. These figures are consistent with further growth in the labor market in October.