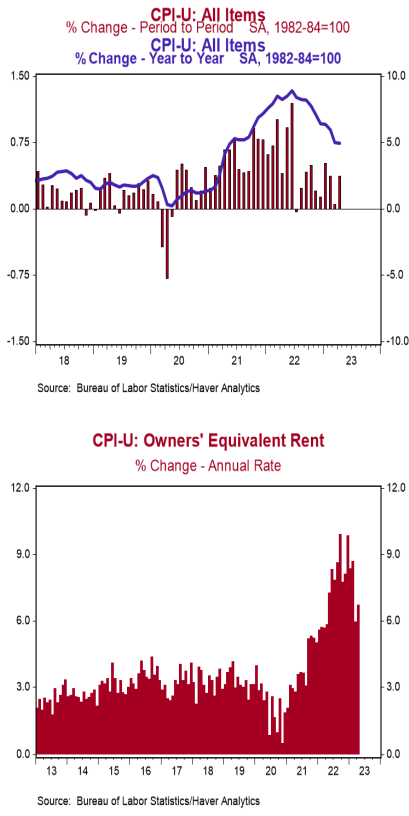

- The Consumer Price Index (CPI) rose 0.4% in April, matching consensus expectations. The CPI is up 4.9% from a year ago.

- Energy prices rose 0.6 % in April, while food prices were unchanged. The “core” CPI, which excludes food and energy, rose 0.4% in April, matching consensus expectations. Core prices are up 5.5% versus a year ago.

- Real average hourly earnings – the cash earnings of all workers, adjusted for inflation – increased 0.1% in April, but are down 0.5% in the past year. Real average weekly earnings are down 1.1% in the past year.

Implications:

Headline inflation re-accelerated in April after a lull in March, and readings remain well above the Fed’s 2% inflation target. For the most volatile categories, energy prices rose 0.6% in April while food prices remained unchanged for a second month in a row. Stripping out these components shows “core” prices rose 0.4% in April, matching consensus expectations. Core prices have risen 5.5% in the past year and have not budged lower on a year-ago basis since the start of the 2023. The main driver within the core categories was once again shelter, which rose 0.4% in April. Rents for both actual tenants and the imputed rental value of owner-occupied homes are running at or above a 6% annualized rate over three-, six-, and twelve-month timeframes. This is important because together they make up a third of the weighting in the overall index. We expect rents to continue to generate high inflation for some time as they catch up to home prices, which skyrocketed in 2020-21. Meanwhile, a subset category of inflation that the Fed is watching closely – known as the “Super Core” – which excludes food, energy, other goods, and housing rents, increased only 0.1% in April. However, the Super Core is still up 5.1% in the past year and has on occasion been slow for a month, followed by a spike upward the following month. Other notable core categories that increased in April were prices for used cars and trucks (+4.4%), motor vehicle insurance (+1.4%), and hospital services (+0.5%). The next two months are going to provide an interesting test for the Federal Reserve, as outsized jumps in inflation that took place in May and June of 2022 begin to roll off of the year-ago comparisons, which could make it look like inflation is moderating rapidly. However – as is often the case – that surge in inflation last year was followed by a lull, with inflation barely budging in July and August 2022. That means we are very likely to see the twelve-month inflation readings re-accelerate toward the end of the summer. Hopefully Powell and Co. look beyond short-term volatility in the data and realize the fight is not finished.