- Real GDP increased at a 2.9% annual rate in Q4, beating the consensus expected 2.6%.

- The largest positive contributions to real GDP growth in Q4 came from inventories and personal consumption. Government purchases, net exports, and business investment in intellectual property were also noticeably positive. The largest drag on Q4 GDP growth was home building.

- Personal consumption, business fixed investment, and home building, combined, rose at a 0.2% annual rate in Q4. We refer to this as “core” GDP.

- The GDP price index increased at a 3.5% annual rate in Q4 and is up 6.3% from a year ago. Nominal GDP (real GDP plus inflation) rose at a 6.5% annual rate in Q4 and is up 7.3% from a year ago.

Implications:

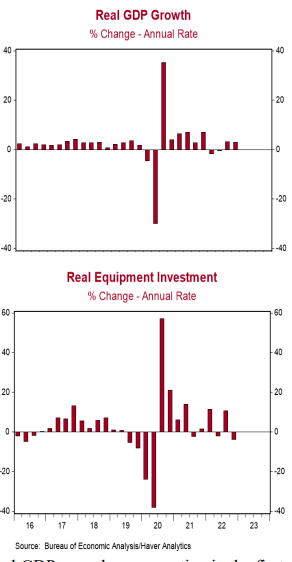

Don’t get used to the solid real GDP report for the fourth quarter; it’s probably the strongest we will see for a while. More recent data for December – including ISM reports, retail sales, industrial production, and housing starts – showed the quarter ended on a sour note and signaled that the first quarter could be negative. Real GDP rose at a 2.9% annual rate in Q4, which is superficially good news. However, about half of the increase in real GDP was due to a rapid accumulation to inventories, which isn’t sustainable and is almost certain to slow by late 2023. Meanwhile, net exports added 0.6 percentage points to the real GDP growth rate in Q4, a factor that has a high risk of going negative in 2023 due to the increase in the dollar’s exchange value in 2022. The two components of real GDP that usually have the most to say about future growth are business investment in equipment and home building, which declined, at 3.8% and 26.7% annual rates, respectively. We like to follow what we call “core” GDP, which includes consumer spending, business fixed investment, and home building. It excludes government purchases, inventories, and international trade, all of which are very volatile from quarter to quarter and which are hard for the US to rely on for long-term growth. Core GDP increased at only a 0.2% annual rate in Q4, a pace that in the past has usually been this low (or worse) just before, during, or just after recessions. Remember how overall real GDP growth was negative in the first half of 2022 but we insisted the US wasn’t in recession? Part of our evidence was that core GDP was still climbing at a respectable pace. Now core GDP growth is near zero, which is why investors need to be concerned. Yes, consumer spending was up at a solid 2.1% annual rate in Q4. But real (inflation-adjusted) wages & salaries are down 0.3% from a year ago, which doesn’t bode well for the quarters ahead. Meanwhile, inflation remains a problem. GDP prices rose at a 3.5% annual rate in Q4 and are up 6.3% from a year ago. Nominal GDP – real GDP growth plus inflation – rose at a 6.5% annual rate in Q4 and is up 7.3% from a year ago. These figures signal that monetary policy needs to remain tight to bring inflation back down.