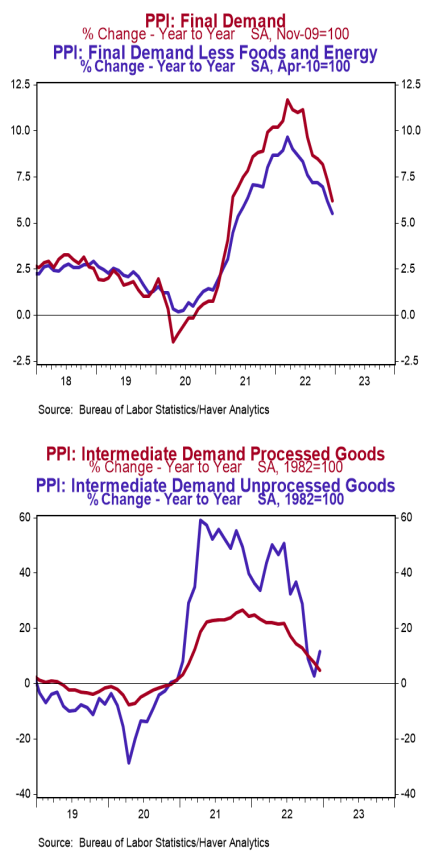

- The Producer Price Index (PPI) declined 0.5% in December, coming in well below the consensus expected -0.1%. Producer prices are up 6.2% versus a year ago.

- Energy prices declined 7.9% in December, while food prices fell 1.2%. Producer prices excluding food and energy rose 0.1% in December and are up 5.5% in the past year.

- In the past year, prices for goods are up 8.0%, while prices for services have risen 5.0%. Private capital equipment prices were unchanged in December but are up 8.7% in the past year.

- Prices for intermediate processed goods declined 2.8% in December but are up 4.7% versus a year ago. Prices for intermediate unprocessed goods rose 3.4% in December and are up 11.7% versus a year ago.

Implications:

Producer prices in December fell the most for any single-month since April 2020, as falling costs for food and energy more than offset rising prices across most other categories. Given the desire by many investors and economic followers alike to latch on to any reason for the Federal Reserve to stop raising rates, the headline number in today’s report will be heralded by some as a sign that inflation has been defeated. And while it certainly does look like peak inflation is behind us, we aren’t popping any champagne bottles just yet. While energy prices fell 7.9% in December and food prices declined 1.2%, “core” producer prices – which remove the typically volatile food and energy categories rose 0.1 % in December and remain up 5.5% in the past year, well exceeding the Fed’s 2% inflation target. Looking deeper into core inflation, prices for both goods (ex-food and energy) and services (+0.2% and +0.1%, respectively) rose once again in December. The service side of the economy will be the key area to watch in 2023. As we have witnessed across many economic reports, the shift back toward the services that were heavily restricted during pandemic shutdowns is driving movement everywhere from employment, to spending, to inflation. We expect the path toward “normal” will be stickier than most anticipate as the economy continues to absorb the massive surge in the M2 measure of money the Fed injected in 2020-21. While there is plenty of prognostication around what the Fed will do and what that means for the economy – and the markets – moving forward, what matters most is that inflation continues to run well above the Fed’s target. Expect a 25 basis point rate hike at the Fed’s meetings in two weeks, along with guidance that the Fed is prepared to continue raising rates further in 2023. The path ahead to tame inflation will test the Fed’s resolve, let’s hope they are up to the task.