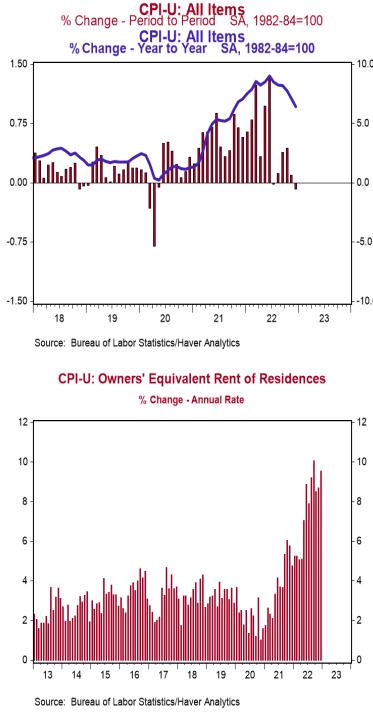

- The Consumer Price Index (CPI) declined 0.1% in December, matching consensus expectations. The CPI is up 6.5% from a year ago.

- Food prices increased 0.3% in December, while energy prices fell 4.5%. The “core” CPI, which excludes food and energy, rose 0.3% in December, also matching consensus expectations. Core prices are up 5.7% versus a year ago.

- Real average hourly earnings – the cash earnings of all workers, adjusted for inflation – increased 0.4% in December, but are down 1.7% in the past year. Real average weekly earnings are down 3.1% in the past year.

Implications:

Consumer prices posted the first monthly decline in two and a half years in December, closing out 2022 on a positive note. While today’s headline decline in prices is a welcome sign of progress and will no doubt be taken as a signal that the Federal Reserve is succeeding in fighting inflation, it’s worth noting just how little progress has been made in the past calendar year. The consumer price index was up 7.0% in the 12-month period ending December 2021 and up 6.5% in the most recent twelve months. No matter which way you cut it, inflation remains well above the Federal Reserve’s target of 2.0%. The largest driver of today’s decline came from the volatile energy sector, specifically the price of gasoline which fell 9.4%. Stripping out energy and its other volatile counterpart, food prices, “core” prices rose 0.3%. While there were a handful of “core” CPI categories that declined for the month, most notably airline fares (-3.1%) and used vehicles (-2.5%), these were offset elsewhere. Housing rents were the main upward driver within the “core” measure, rising 0.8% for the month. We expect housing rent inflation to remain high in 2023 because rents still have a long way to go to catch up to home prices, which skyrocketed during COVID. Some analysts point to “real-time” rental indexes based on what new tenants are paying, which have softened in the last couple of months, as foreshadowing a drop in CPI rents. But this process will take time before they bleed into the CPI, which covers all tenants and homeowners, not just new tenants. Medical care services (0.1%) and auto insurance prices (0.6%) also contributed to “core” inflation in December. While today’s report may be a welcome sign to the markets – make no mistake – the Fed is not out of the woods. Much of the progress we have seen in the past few reports has come from volatile categories like energy which could come bouncing back just as rapidly. Inflation has now migrated from the goods sector into services which is what we will be closely watching in 2023. Finally, initial unemployment claims fell 1,000 last week to 205,000, while continuing claims declined by 63,000 to 1.634 million. These figures are welcome news on the labor market, but New Year’s Day was on a Monday last week and could have affected the seasonal adjustments.