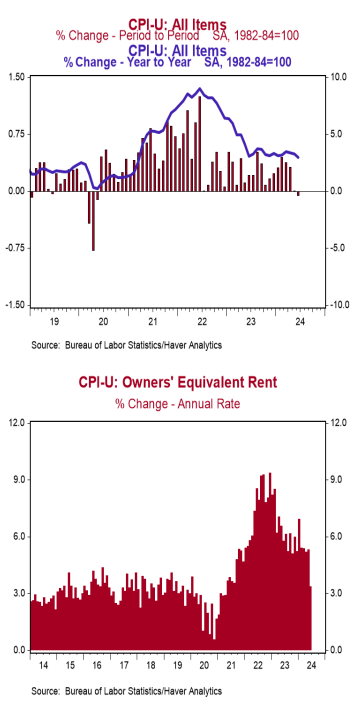

The Consumer Price Index (CPI) declined 0.1% in June, below the consensus expected +0.1%. The CPI is up 3.0% from a year ago.

Energy prices declined 2.0% in June, while food prices rose 0.2%. The “core” CPI, which excludes food and energy, rose 0.1% in June, below the consensus expected +0.2%. Core prices are up 3.3% versus a year ago.

Real average hourly earnings – the cash earnings of all workers, adjusted for inflation – rose 0.4% in June and are up 0.8% in the past year. Real average weekly earnings are up 0.6% in the past year.

Implications: Inflation came in softer than expected for the third straight month in June, posting the first outright monthly decline since the early months of COVID. This will add to the Federal Reserve’s confidence that inflation, still running at 3.0% on a year-ago comparison basis, is eventually heading back down to the 2.0% target, which means cuts in short-term interest rates are likely to start in September. Looking at the big picture, there was considerable progress against inflation from mid-2022 to mid-2023: consumer prices were up 9.1% in the year ending in June 2022 and then dropped rapidly back to 3.0% in the year ending in June 2023, leading many to believe the end of “temporary” pandemic inflation problems was in sight. But then inflation pressures reignited in the first quarter of this year, casting doubt on the Fed’s ability to cut rates in 2024. Now it appears that inflation has resumed its downward trend, a lagged response to the drop in the M2 measure of money compared to early 2022. Looking at the details of today’s report, June inflation was held down by energy prices, which declined 2.0% on the back of lower prices for gasoline (-3.8%). Stripping out energy and its often-volatile counterpart (food), “core” prices also came in softer than expected, rising 0.1% for the month, the smallest advance since August 2021. Within the core categories, the most notable movement came from a slowdown in housing rents. The two categories that make up housing rents – those for actual tenants as well as the imputed rental value of owner-occupied homes – increased 0.3% in June, their smallest advances since 2021. Housing rents have been a key driver of inflation over the last couple years and their trajectory will have important implications for the future path of inflation as they make up a third of the overall index. Meanwhile, a subset category of prices the Fed has told investors to watch closely and is a useful gauge of inflation in the service sector – known as the “Supercore” – which excludes food, energy, other goods, and housing rents, declined 0.1% in June. That is the first outright decline since August 2021, a welcome sign for the Fed as Supercore has showed little sign of abating since the Fed began hiking rates. Other notable categories to decline in June include prices for airfare (-5.0%), hotels (-2.5%), used vehicles (-1.5%), and new vehicles (-0.2%). In other news today, initial unemployment claims declined 17,000 last week to 222,000. Continuing claims decreased 4,000 to 1.852 million.