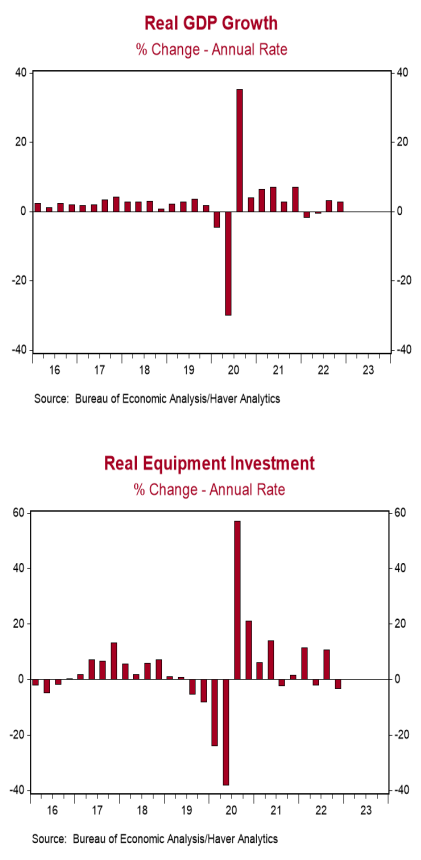

- Real GDP growth in Q4 was revised lower to a 2.7% annual rate from a prior estimate of and consensus expected 2.9%.

- Downward revisions to consumer spending and net exports more than offset upward revisions to business investment, and home building.

- Personal consumption, business fixed investment, and home building, combined, rose at a 0.1% annual rate in Q4. We refer to this as “core” GDP.

- The GDP price index was revised up to a 3.9% annual growth rate from a prior estimate of 3.5%. Nominal GDP growth – real GDP plus inflation – was revised up to a 6.7% annualized rate from a prior estimate of 6.5%.

Implications:

Today’s second report on fourth quarter GDP can be summed up in a few words, less consumer spending and higher prices. Real GDP was revised lower from the initial reading a month ago, growing at a 2.7% annual rate. The downward revision to the overall number was due to weaker consumer spending and lower net exports, which more than offset upward revisions to business investment in structures and intellectual property, and home building. To analyze the growth trends more accurately, we follow "core" GDP, which includes consumer spending, business fixed investment, and home building, while excluding government purchases, inventories, and international trade, which are too volatile for long-term growth. Unfortunately, core GDP increased at a meager 0.1% annual rate in Q4, which is even lower than the previous estimate of 0.2% a month ago. This pace is alarming as it usually precedes, accompanies, or follows a recession. Regarding monetary policy, today’s inflation news shows the Federal Reserve has more work to do. GDP inflation was revised higher to a 3.9% annual rate in Q4 versus a prior estimate of 3.5%. GDP prices are up 6.3% from a year ago, nowhere near the Fed’s 2.0% target. Meanwhile, nominal GDP (real GDP growth plus inflation) rose at a 6.7% annual rate in Q4 and is up 7.4% from a year ago. In other news today, initial unemployment claims fell 3,000 last week to 192,000, while continuing claims declined by 37,000 to 1.654 million. Expect another solid payroll report for February, but not near as strong as January.