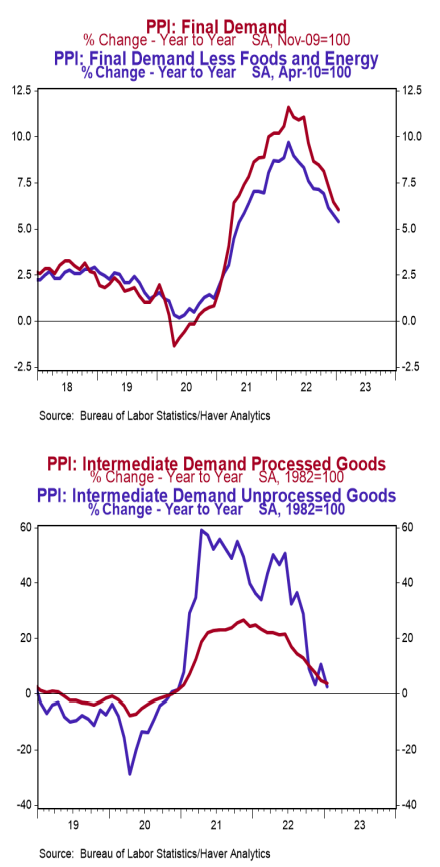

- The Producer Price Index (PPI) rose 0.7% in January, coming in well above the consensus expected +0.4%. Producer prices are up 6.0% versus a year ago.

- Energy prices rose 5.0% in January, while food prices fell 1.0%. Producer prices excluding food and energy increased 0.5% in January and are up 5.4% versus a year ago.

- In the past year, prices for goods are up 7.5%, while prices for services have risen 5.0%. Private capital equipment prices rose 0.4% in January and are up 7.7% in the past year.

- Prices for intermediate processed goods rose 1.0% in January and are up 3.8% versus a year ago. Prices for intermediate unprocessed goods declined 5.0% in January but are up 2.3% versus a year ago.

Implications:

Producer prices snapped back from a December decline to rise 0.7% in January, as costs rose virtually across the board. As with the CPI report released this past Tuesday, today’s inflation check reinforces the Fed’s conviction that the battle against inflation is far from over. While it certainly does look like peak inflation is behind us, prices continue to rise at a stubbornly quick pace that is causing at least one Fed member to question if discussions should be less on when the Fed can pause hikes, and more on if a return to 50 basis point moves is appropriate. Taking a look at the details of today’s report shows that goods prices – specifically energy – led the way in January, rising 1.2%. Energy prices increased 5.0% in January as natural gas, diesel, and jet fuel costs all rose, while food prices declined 1.0% on the back of softening prices for vegetables. Removing these typically volatile food and energy categories shows “core” producer prices rose 0.5% in January and remain up 5.4% in the past year, far exceeding the Fed’s 2% inflation target. While goods prices were the key factor lifting inflation in January, this is a departure from the recent trend of services taking charge. We believe the service side of the economy is the key area to watch in 2023 and the Fed seems to agree, with Chair Powell noting at the most recent Fed press conference that while supply-chain easing is moderating goods inflation, it is services that has the Fed cautious about claiming any sort of victory. We expect the path toward the Fed’s 2% target will prove stickier than most anticipate as the economy continues to absorb the massive surge in the M2 measure of money the Fed injected in 2020-21. Higher rates – and the economic slowdown that will accompany – are the price we pay for the “sugar high” of stimulus we enjoyed in 2020 and 2021.