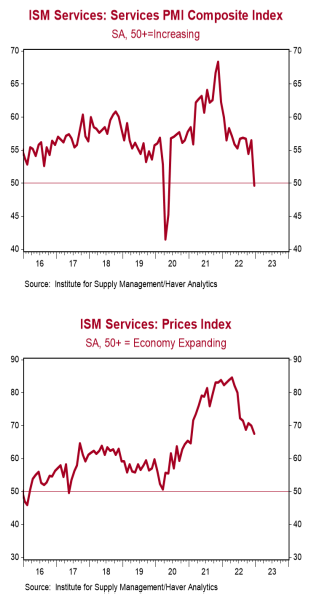

- The ISM Non-Manufacturing index dropped to 49.6 in December, well below the consensus expected 55.0. (Levels above 50 signal expansion; levels below signal contraction.)

- The major measures of activity were all lower in December. The business activity index fell to 54.7 from 64.7, while the new orders index dropped to 45.2 from 56.0. The employment index declined to 49.8 from 51.5, while the supplier deliveries index decreased to 48.5 from 53.8.

- The prices paid index declined to 67.6 in December from 70.0 in November.

Implications:

The ISM Services index surprised sharply to the downside for December, now matching the ISM Manufacturing index in contraction (below 50) territory. Looking at the survey comments, companies cited a general slowdown in orders. That can be seen in the movement from the new orders index, which dropped to 45.2 from 56.0 in November. The business activity index also dropped a sharp ten points, but remains in expansion territory at 54.7. While it’s clear that businesses and consumers have been shifting resources away from goods and toward the still re-opening service sector, tighter monetary conditions appear to be finally weighing on the sector that has led the US economy higher in 2022. We believe the US economy will enter recession sometime in 2023, as the bill for the massive artificial stimulus of 2020-21 comes due. In terms of the details, the employment index fell back into contraction territory in December. Comments from employers show that some companies are starting to tighten hiring of new employees due to uncertainty about the strength of the economy in 2023. One piece of good news from today’s report was the supplier deliveries index fell below 50 for the first time since 2019, signaling shorter wait times. Finally, the prices paid index declined to a still elevated 67.6. While that is well below its peak from earlier this year – make no mistake – inflation is still a major problem in the service sector, with fifteen (out of eighteen) industries reporting paying higher prices in December. We expect the service sector to keep inflation trending well above the Fed’s 2.0% target for some time. For now, the service sector remains a source of strength in the US economy. Eventually, the bill will come due for the policy decisions that were made in the last few years. There is no such thing as a free lunch.